We expect the ALP’s proposed policy change to franking credit refunds to have the following major implications for investors:

At the margin, drive a minor de-rating of high yield/highly franked stocks vis-à-vis high yield/low or no franked stocks as the loss of the tax kicker is priced in. However, because retail investors are not the only price setter, we don’t expect this to be meaningful;

Raise the attraction of high yield/highly franked stocks which have stronger earnings and dividend growth prospects as investors increasingly look at total return (growth plus yield) over just income – see table 1 for a full stock list. In addition, stocks where dividend payout ratios might already be high and/or unsustainable could also suffer from selling pressure;

A de-rating of Tier 1 hybrids and Listed Investment Companies (LICs). Part of this discounting appears to have already taken place, but more can be expected should the market perceive an increasing chance of proposed policy becoming legislation;

Hybrid issuers to raise the yield (reducing their own margins) to offset any weaker demand as they attempt to provide greater compensation for a loss of tax benefits. Expect to see a continuation of the trend to issue Listed Investment Trusts versus LICs.

We expect a continuation of capital management activity from corporates as they rush to empty excess franking credit balances. In the short-term, this means that not all fully franked dividend yield paying stocks carry the same near-term downside risk. This is clearly positive for short term income seekers but distributing excess franking credits also comes at a cost of lowering capital investment, potentially impacting future growth options.

We don’t expect proposed policy changes to drive immediate asset allocation shifts. However, short term policy changes add to structural drivers that are already affecting domestic asset allocation trends. Retail investors are too overweight Australian equities and dividend yield stocks at the expense of fixed income and international equities and over the medium to longer term we expect these structural portfolio imbalances to be increasingly addressed.

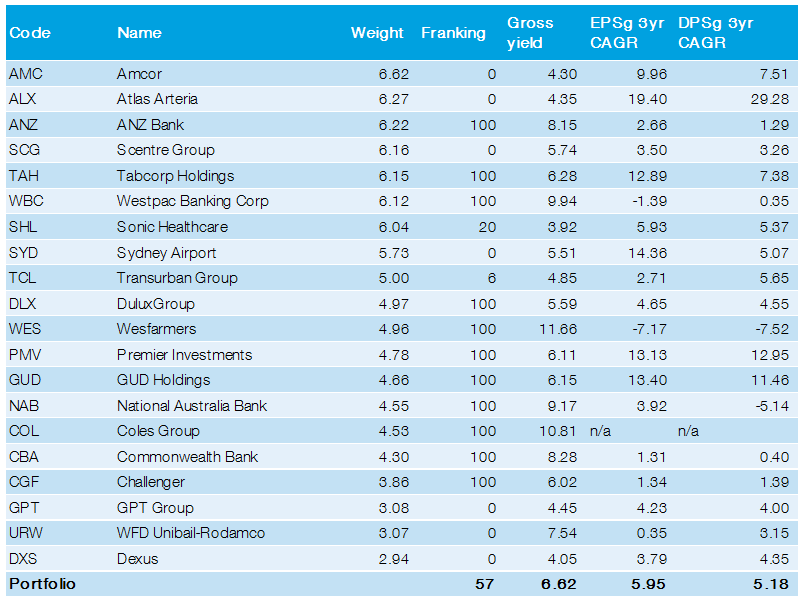

Fully franked dividend payers provide little dividend growth (S&P/ASX 50)

Source: Macquarie Research, MWM Research, March 2019

Our key recommendations should this policy proposal become law are as follows:

Those investing for total return should consider selling high yield / low growth stocks and be prepared to add stocks with lower yield but higher earnings / dividend growth opportunities. Similarly, stocks where the payout ratio has the capacity to increase could also provide incremental income. International equities or high-growth ASX stocks (see table 2 and 3) should also be considered.

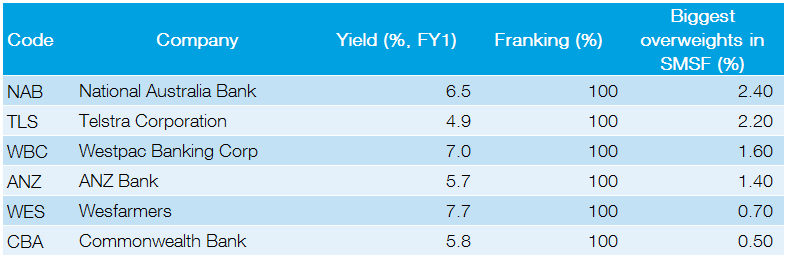

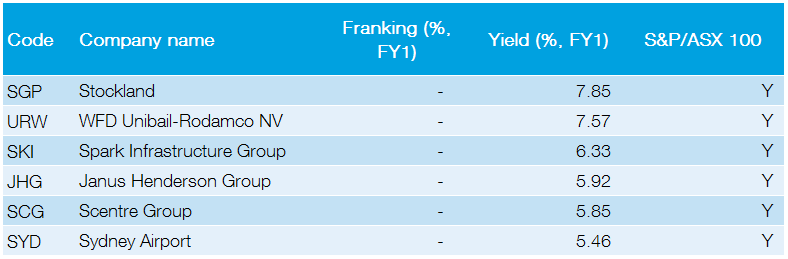

Investors overly exposed to franking credits could consider reweighting to stable dividend payers with lower franking such as REITs, infrastructure and offshore earners (see table 1 S&P/ASX 50 stocks). This should also reduce portfolio volatility by providing diversification away from financials towards more defensive (longer duration) sectors.

For those considering adding managed income funds to supplement income from direct equities, we recommend the Nikko AM Australian Share Income Fund and the PIMCO Income Fund within Australian equities and fixed interest respectively.

What's the proposal?

The Australian Labor Party (ALP) recently announced a proposal to remove franking credit refunds. Exempt from this proposed policy change would be:

Charities;

Not-for-profit institutions; and

Age pensioners and allowance recipients, including SMSFs with at least one pensioner/allowance recipient prior to March 2018.

At this point, the ALP has stated that the intention is to implement the proposal by 1 July 2019 with no grandfathering.

To date, the focus of much of the discussion has been on the negative consequences for some investors depending on their taxable income due to the removal of the franking credit refund. However, there are broader implications including for corporates, the overall listed market as well as individuals and superannuation funds.

What are the key impacts should the proposal become legislation?

Stock price and asset allocation impacts for individual investors with taxable income brackets lower than the corporate rate and superannuation funds are impacted negatively from an income perspective. We expect that we would see some short-term volatility as these investors reassess the value of highly franked/high dividend stocks. However, historically, policy driven spikes in volatility tend to be short lived, with the market typically finding an equilibrium.

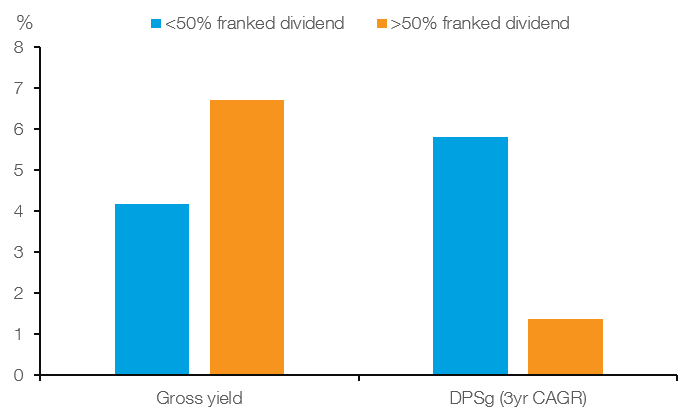

We expect it to be negative for high yield/high franking stocks relative to stocks with little or no franking as investors reprice stocks for the loss of the tax benefit, but because retail investors are not the only price setter for high yield stocks, we don’t expect the impact to be particularly large.

Stocks most likely to be impacted negatively

High yield stocks that don't pay franking

Source: Macquarie Research, MWM Research, March 2019

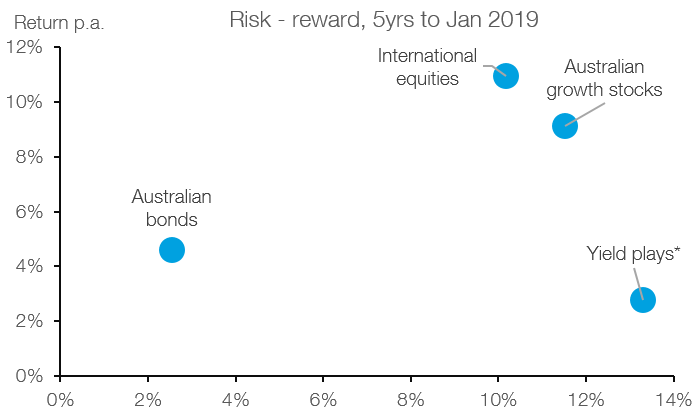

Over the medium to longer term, we expect to see proposed policy changes will add to structural forces driving asset allocation changes for domestic investors. In all likelihood, investors will look to increase allocations to fixed income in order to maintain yields and towards international equities for exposure to growth assets. This should be viewed as a positive given total risk-adjusted returns are likely to improve as investors move to a more balanced versus yield focused portfolio.

Adding growth stocks and fixed income leads to portfolios with superior risk-reward

*equal weight portfolio of ANZ, CBA, NAB, WBC, WES, WOW.

Source: Morningstar, Macquarie Research, March 2019.

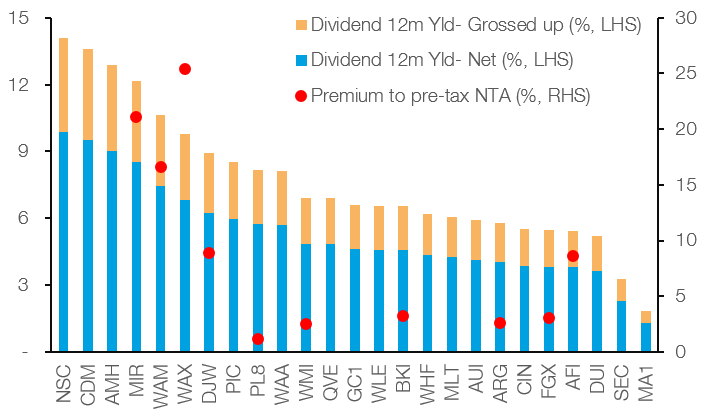

Listed Investment Companies (LICs) have been a popular investment vehicle (particularly for SMSFs) partly due to 100% franking. We believe Australian equity LICs trading at a premium and valued on their dividend yield would be most at risk of a sell-off. Based on our analysis, Mirrabooka (MIR), WAM Capital (WAM), WAM Research (WAX) and Djerriwarrh Investments (DJW) look most vulnerable due to each trading on substantial premiums and offering fully franked yields of up to 10%.

It already appears that a transition is underway from LICs towards Listed Investment Trusts (LITs) judging by recent issuance. This trend will likely gather steam if it appears that the proposed policy is likely to be implemented.

LICs trading at a premium with fully franked yields are likely to reprice most

Source: Iress, MWM Research, March 2019

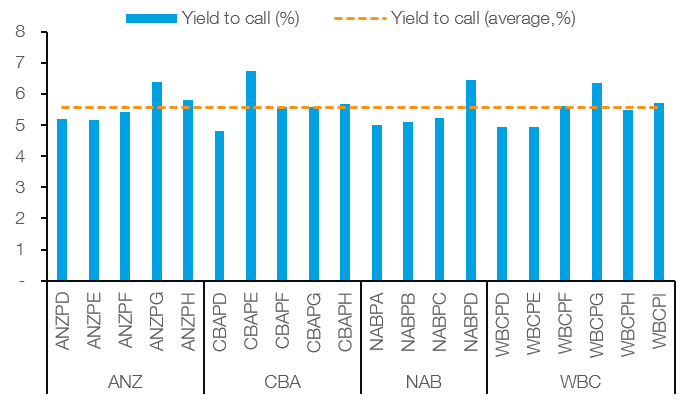

Hybrid valuations and demand will also likely come under downward pressure, particularly Tier 1 hybrids given the high participation of SMSFs. We believe this could be further exacerbated by low liquidity in these markets. Key to our expectation that Tier 1 hybrids will reprice lower is that this change, were it to become legislation, will not be a tax event which means issuers are not obligated to redeem the security. Issuers are also unlikely to provide any offset in our view. We would expect that the traded margin will widen on existing issues and for any new issues that come to market, to be offered at higher yields as investors demand compensation for the loss in the tax pickup.

Higher yields are expected for Tier-1 hybrid securities

Source: Iress, MWM Research, March 2019

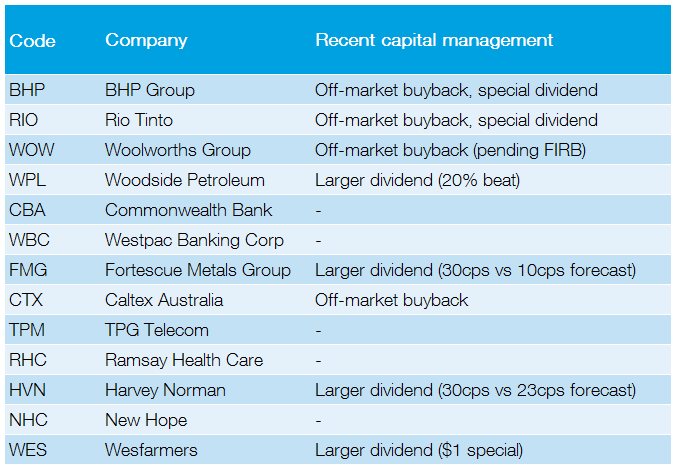

In our view, Australian corporates will continue to empty franking credit balances, which has already begun via off-market buybacks and special dividends. Most recently, we have seen Fortescue (FMG), Rio Tinto (RIO) and Wesfarmers (WES) surprise the market with special dividends, all fully franked, while Woolworths (WOW) promised an off-market buyback following the sale of its petrol division. This followed off-market buybacks from BHP/RIO and a large dividend increase from Harvey Norman (HVN) last year.

Capital management to pick-up

Source: MWM Research, March 2019

Further capital management appears likely if the policy comes into play. Macquarie analysts believe HT&E Ltd, Oz Minerals, Nick Scali, Premier Investments, Commonwealth Bank also have the potential to take action on their large franking balances.

What can investors do?

There are several options available for investors to offset the potential impacts from Labor’s proposed targeting of franking credits, but we urge caution in rushing to make changes. These changes are dependent on Labor coming into government and the policy being fully implemented. Similarly, individuals should consider the reaction function of corporates via potential special dividends / buybacks which could serve to provide a near term income boost. In other words, the level of uncertainty around policy, its timing and the reaction function by both corporates and investors suggest that understanding the broad implications and not just those that stem from reduced dividend income will be important as the path to (potential) implementation becomes clearer. We summarize the four major options for offsetting franking credit policy below:

Restructuring existing portfolios to reduce reliance on securities paying franking dividends.

Shifting funds away from SMSFs and into APRA-regulated funds in a net tax-paying position appears one of the most likely behavioural responses. This could entail the entire SMSF balance or just the portion allocated to Australian equities. The parliamentary budget office (PBO) believes this response from SMSFs would be the most material, particularly in earlier years, with the revenue gain from SMSFs ~20% higher in the first year in the absence of this response.

Retirees with an SMSF structure may invite tax-paying members to their fund, such as their children, to utilise franking credits to offset income from contributions and investments. However, the PBO expects this will have a low take-up given people tend to prefer managing their financial affairs privately.

- Similarly, couples are expected to shift share ownership away from the lower-income earner to the higher-income earner to fully utilise non-refundable credits.

Overall, we don’t think the proposed policy changes are something that will have a large impact on the equity market. However, it will raise the attractiveness of high yield stocks that don’t pay franking vis-à-vis those that do for a small group of investors. We think Hybrids and LIC’s will be most negatively impacted given high SMSF participation and where they sit in the capital structure. We believe franking credit changes will not, in isolation, drive large scale asset allocation shifts but they will add to the structural drivers that are pushing driving greater weightings towards fixed income and international equities.

Appendix

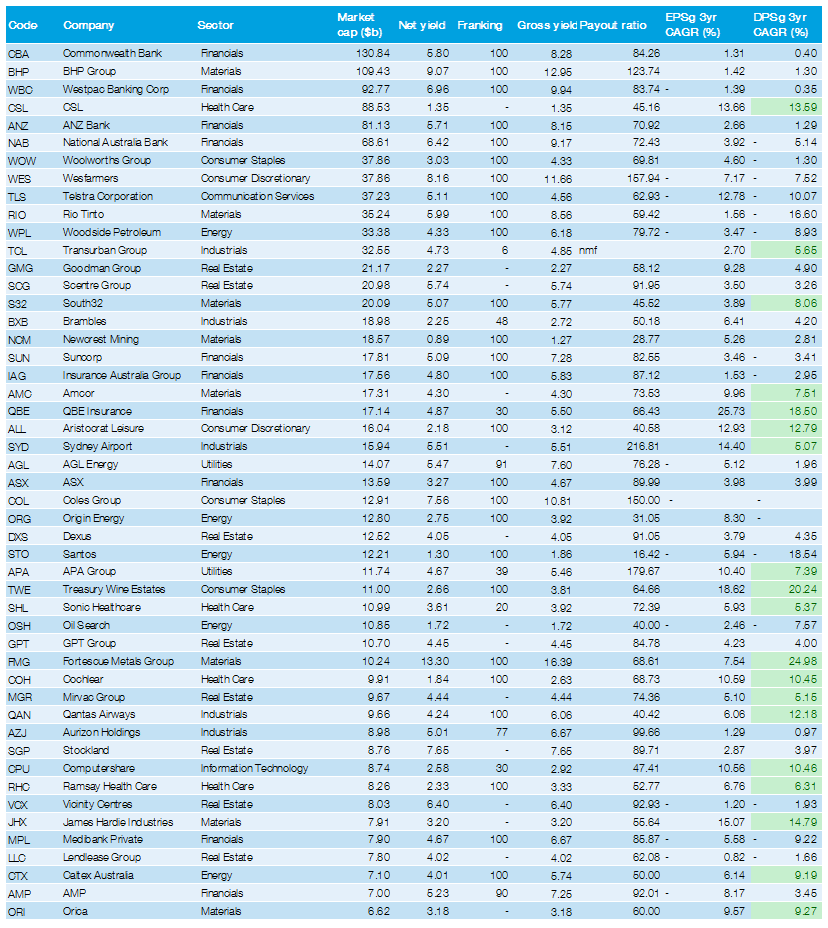

Table 1: S&P/ASX 50 stocks, ranked by market cap. Dividend growth >5% highlighted.

Source: Macquarie Research, MWM Research, March 2019

Table 2: Listed Growth Portfolio

Source: Macquarie Research, MWM Research, March 2019

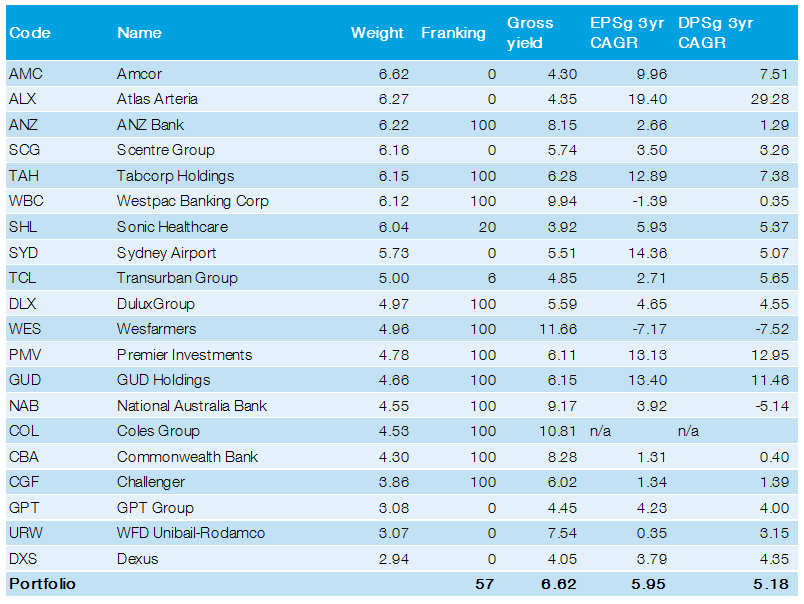

Table 3: Listed Income Portfolio