New Macquarie research reveals the surprising truth behind client satisfaction, with important insights for every advice practice.

Outstanding client relationships are at the centre of every successful advisory business. But while we all understand the importance of client satisfaction, identifying the activities that have the greatest impact on engagement can be more challenging. According to Sherise Mercer, Head of Market Development for Macquarie's Virtual Adviser Network, the problem for most practices is simply a lack of reliable information.

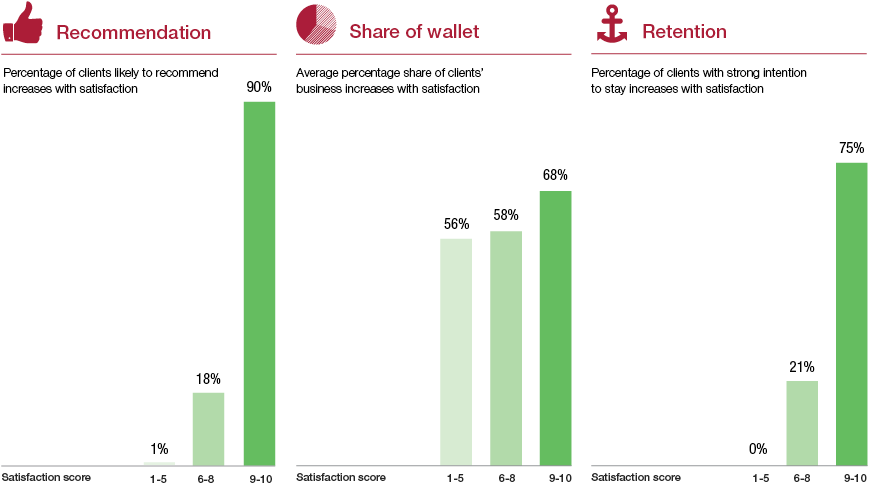

"Often advisers lack the data they need to accurately measure current client engagement levels and identify the factors that could drive them higher in the future," she says. "That's important, because there is a very clear link between higher satisfaction and improved business outcomes, especially retention, referral and share of wallet. Without accurate data, it can be very hard to target business improvement initiatives where they will be most effective."

"Essentially, you can end up spending a great deal of time and money on activities that simply don't have the impact you expect."

To help solve that problem, Mercer and her team created the Propensity Project – an in-depth analysis of advice practices and their clients across Australia. By measuring client engagement and benchmarking practices against their peers, the project aimed to give advisers the insights they needed to make more informed strategic decisions and achieve a higher return on investment.

The results not only highlight the importance of satisfaction for sustainable success, they also reveal that the true drivers of satisfaction are often very different to those on which advisers have traditionally focused.

Understanding what makes clients tick

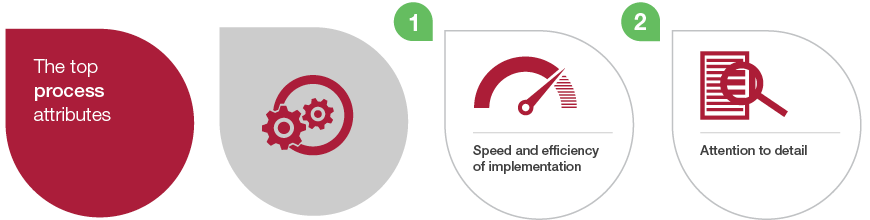

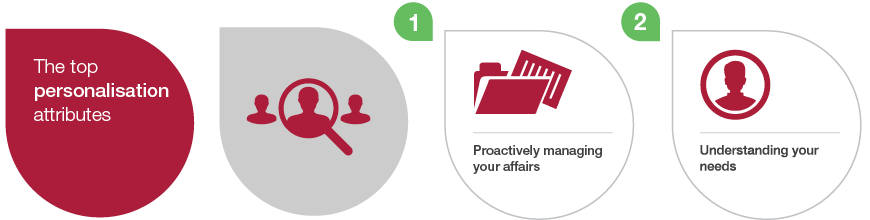

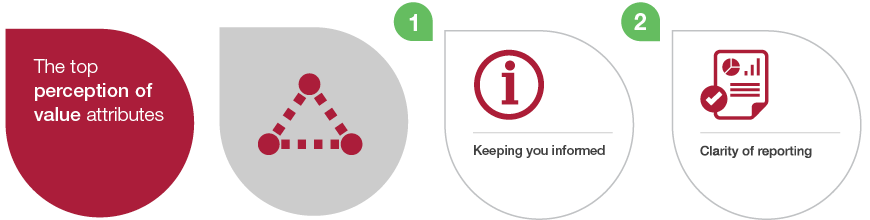

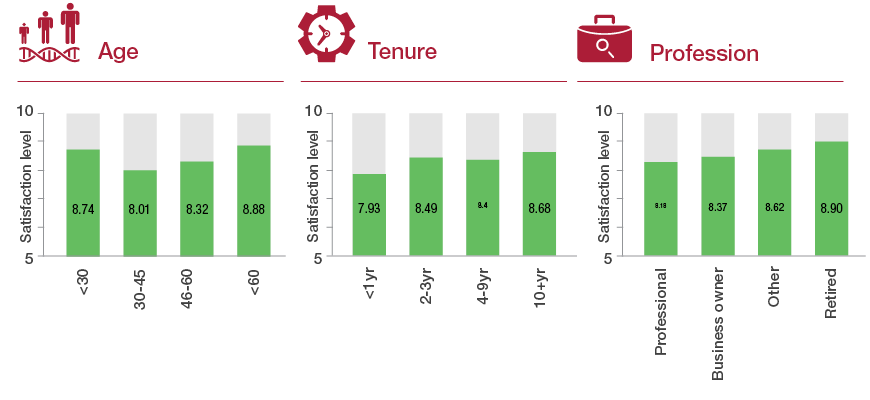

The Propensity Project was based on an in-depth survey of 1,283 clients across 21 financial advice and accounting practices in June and September 2014. The Project team measured client engagement across multiple aspects of each practice's service offering. Then, using advanced statistical analysis, they identified specific drivers of engagement and key factors in creating stronger client relationships.

As well as measuring overall performance across the adviser population, the project also identified benchmarks for key service attributes, representing the best score achieved by any practice for that individual measure. By identifying best practice benchmarks, the Project team was able to uncover the characteristics that made the best performers stand out from the rest – with valuable insights for every advice business.