A couple will need $60,457 per annum to fund a comfortable lifestyle in retirement, assuming they own their own home and have no debt. A single person would need $44,011 per year.

These are the numbers the Association of Superannuation Funds of Australia (ASFA) released for the September 2017 quarter1 as part of its ongoing ASFA Retirement Standard benchmark monitoring. Refer to the ASFA Retirement Standard for information about the budget breakdowns that support these numbers.

In a media release2 dated 4 December 2017, ASFA indicated that a couple needs approximately $640,000 to fund a comfortable retirement, and $545,000 for a single person.

So how can the income required for a comfortable retirement be funded, and how much should be put aside each year prior to retirement to accumulate the funds required to fund a comfortable retirement? The following analysis is intended as a guide for financial services professionals to help their clients set attainable retirement goals.

Funding a comfortable retirement

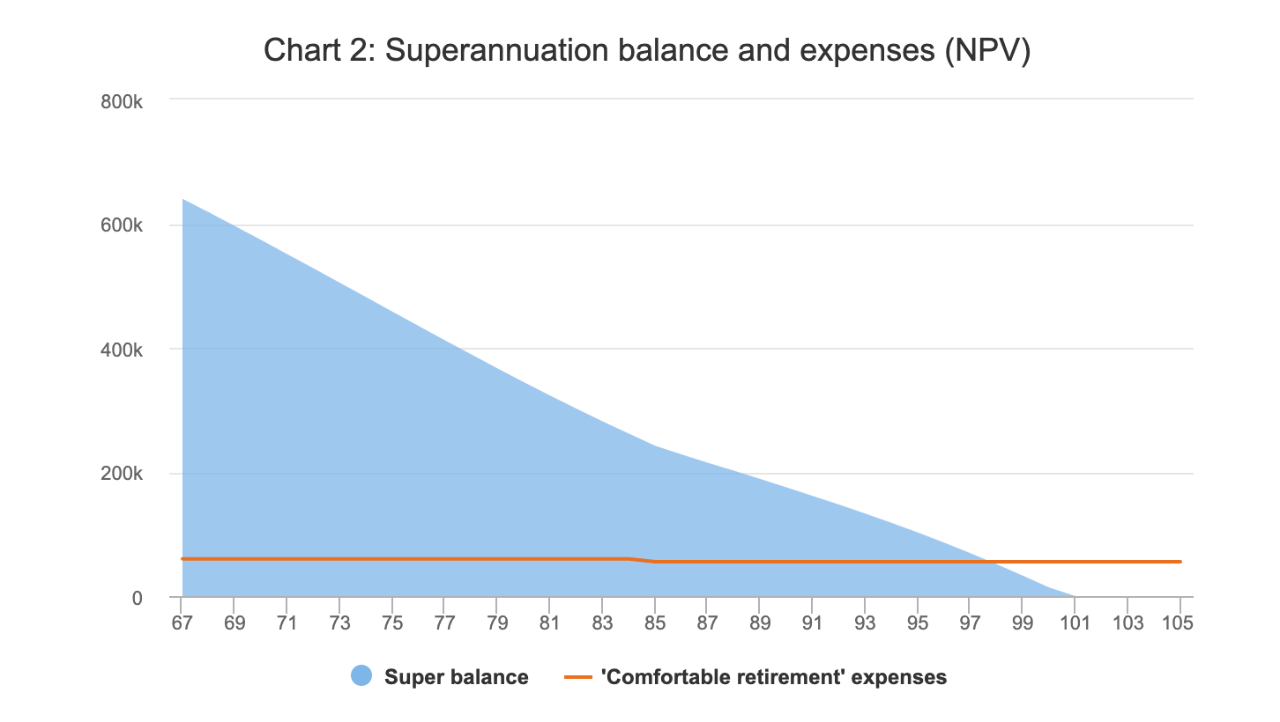

ASFA calculates that $640,000 is sufficient to fund a comfortable retirement lifestyle. Their calculations assume a couple owns their own home and will receive Government age pension support when they retire.

Macquarie Technical Services has modelled the retirement income for a couple in this situation based on the current income tax and social security rates and thresholds. The latest rates and thresholds can be accessed in Macquarie Technical Services' Little Black Book.

It is assumed that $640,000 is held in a superannuation fund and used to commence an account-based pension. Note however that if the funds were held outside super in joint names, there wouldn't be any significant change in the outcome, as the couple are unlikely to pay any income tax on the portfolio returns, based on our return assumptions (see Appendix) and the current income tax law. Nor would their social security entitlements change. It is also assumed that the couple's home contents and car are valued at $25,000.

Chart 1 below shows the projected position of this couple from age 67 to age 106. The couple draw only what they need from their superannuation account-based pension to top up to their age pension income to the required level of total income for a comfortable retirement. The level of income needed, based on ASFA's model, decreases from approximately $60,000 per year prior to age 85, to approximately $55,000 per year - this reflects a relatively less active lifestyle as age increases.

Although their age pension entitlement is just $12,000 (approx.) per annum in the first year, that entitlement grows over time as their assets reduce - the couple become entitled to the full age pension from age 91.

This outcome is sensitive to the earnings rate assumption (6.7 per cent per annum). ASFA's assumption of 7.0 per cent per annum increases the age to which the income level can be maintained by a year, to age 100.

Other sensitive assumptions include the amount of non-financial assets ($25,000) and financial assets, for example cash holdings ($nil). These assumptions may affect the couple's age pension entitlement, hence the amount of pension payments that need to be drawn from the account-based pension. But note that financial assets may have a net positive impact due to the additional income produced.

Our modelling supports ASFA's proposition that approximately $640,000 is an appropriate level of funds for a couple to target for a comfortable retirement, if we accept that approximately $60,000 per annum is needed to achieve that.

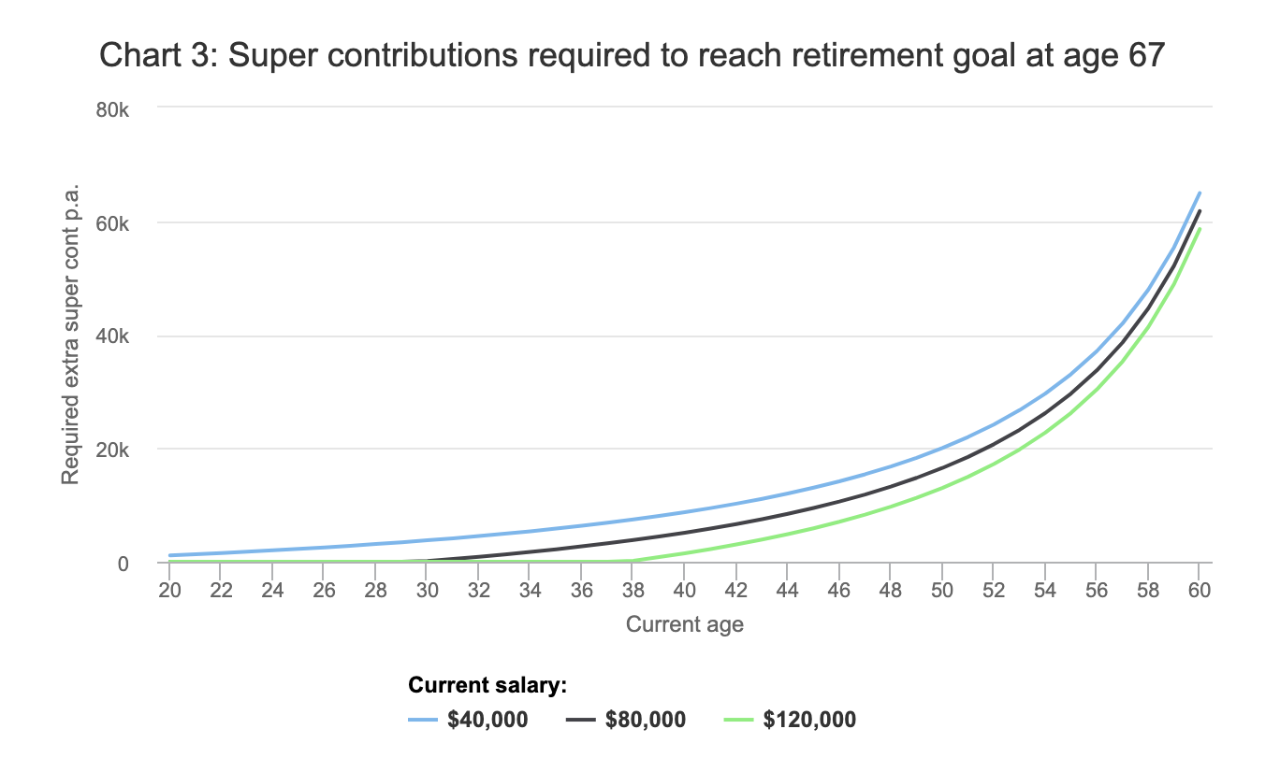

Saving for a comfortable retirement

Taking ASFA's numbers ($640,000 for a couple, $545,000 for singles) as appropriate funding targets, then a natural subsequent question is: