The rapid momentum in house price growth may be showing signs of slowing as affordability becomes tougher for some buyers. Despite these indicators, there is still optimism in Australia’s residential market – which is good news for investors, homeowners and business owners.

In our second quarterly property market update webinar, Macquarie Business Banking’s acting National Real Estate Segment Head, Stuart Hobden, discussed the current market forces with CoreLogic’s Research Director, Tim Lawless.

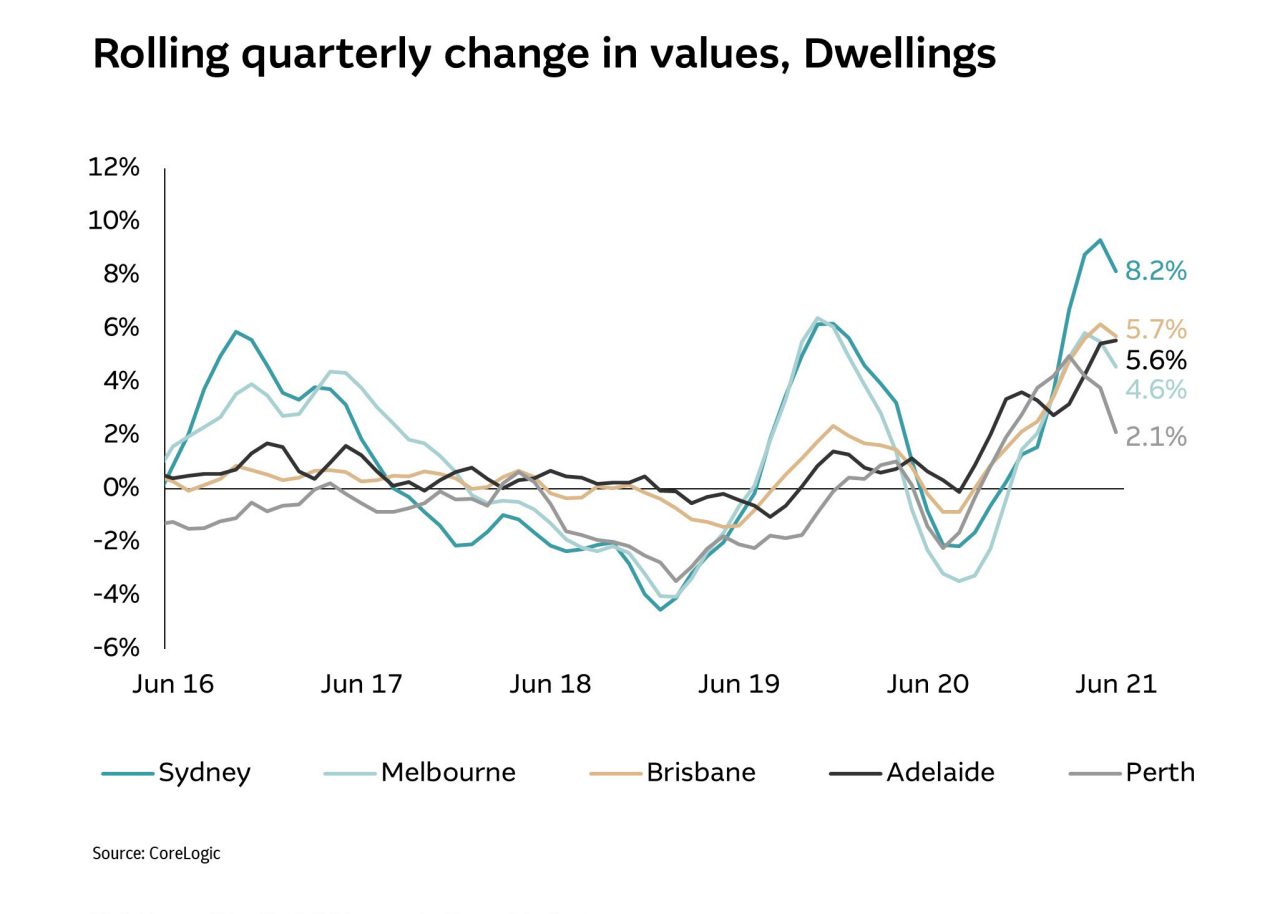

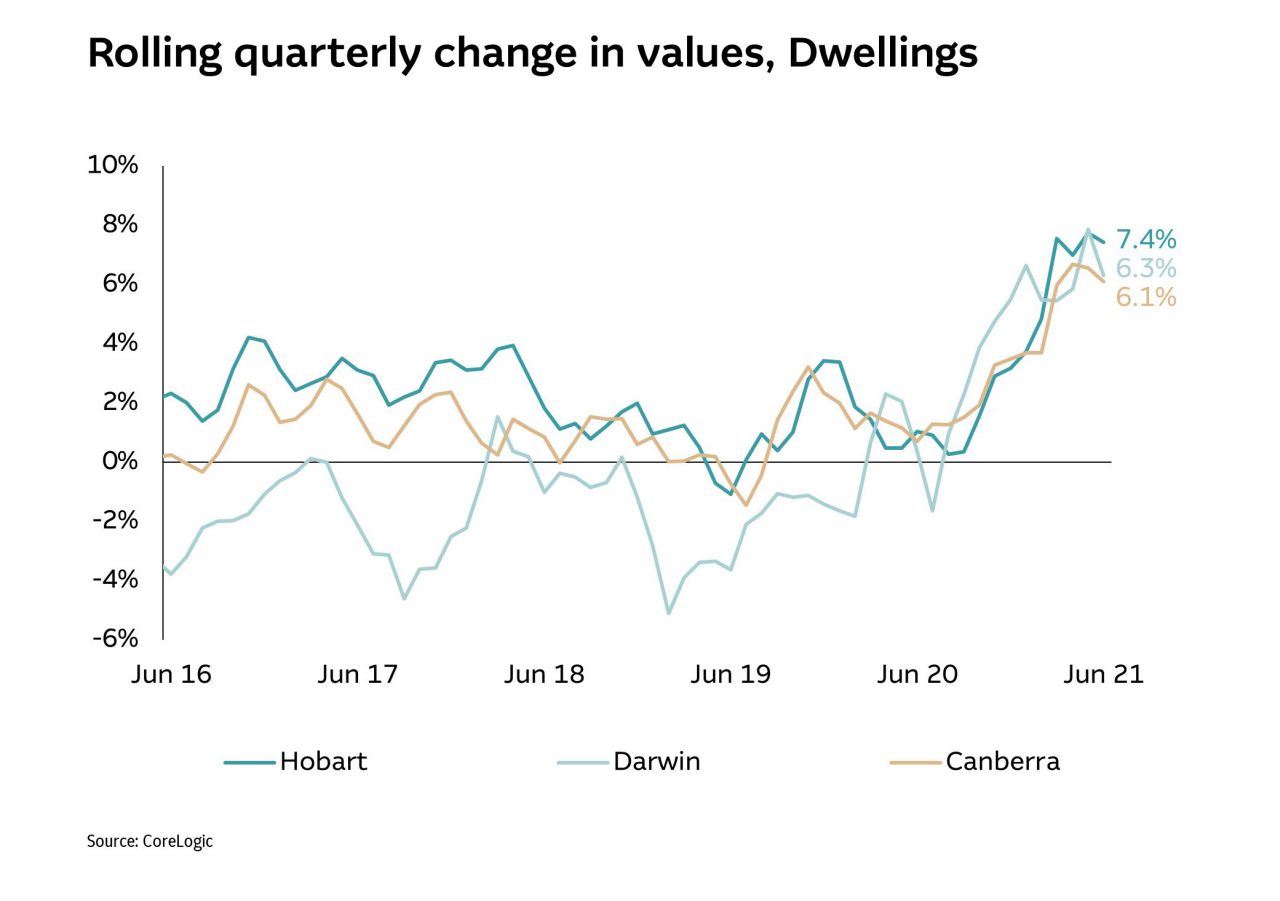

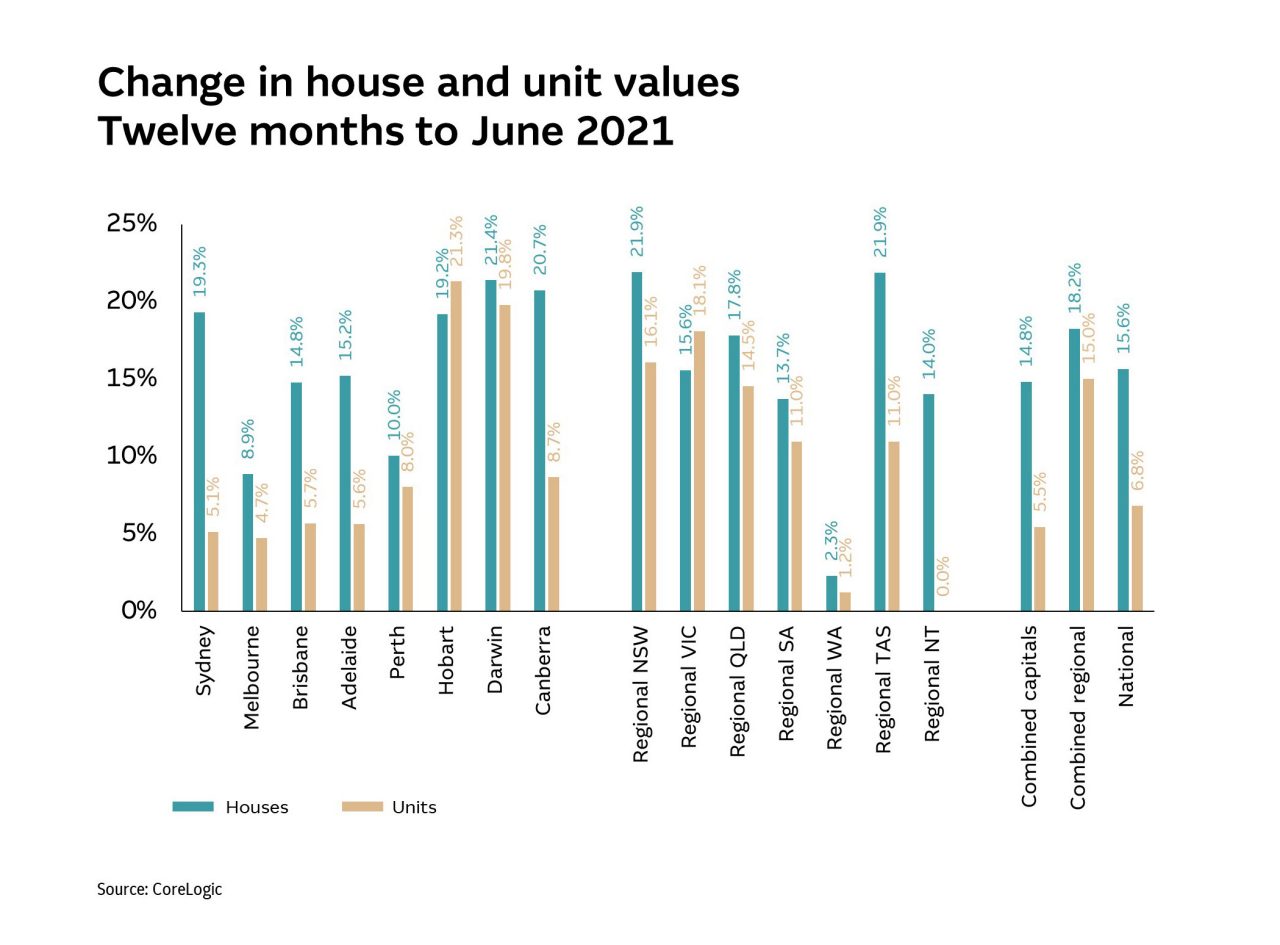

It’s hard to find any region in Australia where house values haven’t climbed well above average levels. Sydney has led the pace of strong capital gains, with values rising 15% in the past 12 months, including an 8.2% uplift in the last quarter alone, and we’re seeing growth across the board – Darwin’s annual growth is 21%, while Canberra and Hobart are up 18% and 19.6% respectively.

However, in recent months the pace of growth has eased. Tim believes affordability constraints will become a bigger hurdle for many prospective buyers – including first-home buyers.

“As house prices rise at a substantially faster pace than household incomes, saving for a deposit and funding transaction costs are becoming larger barriers to entry,” he said.

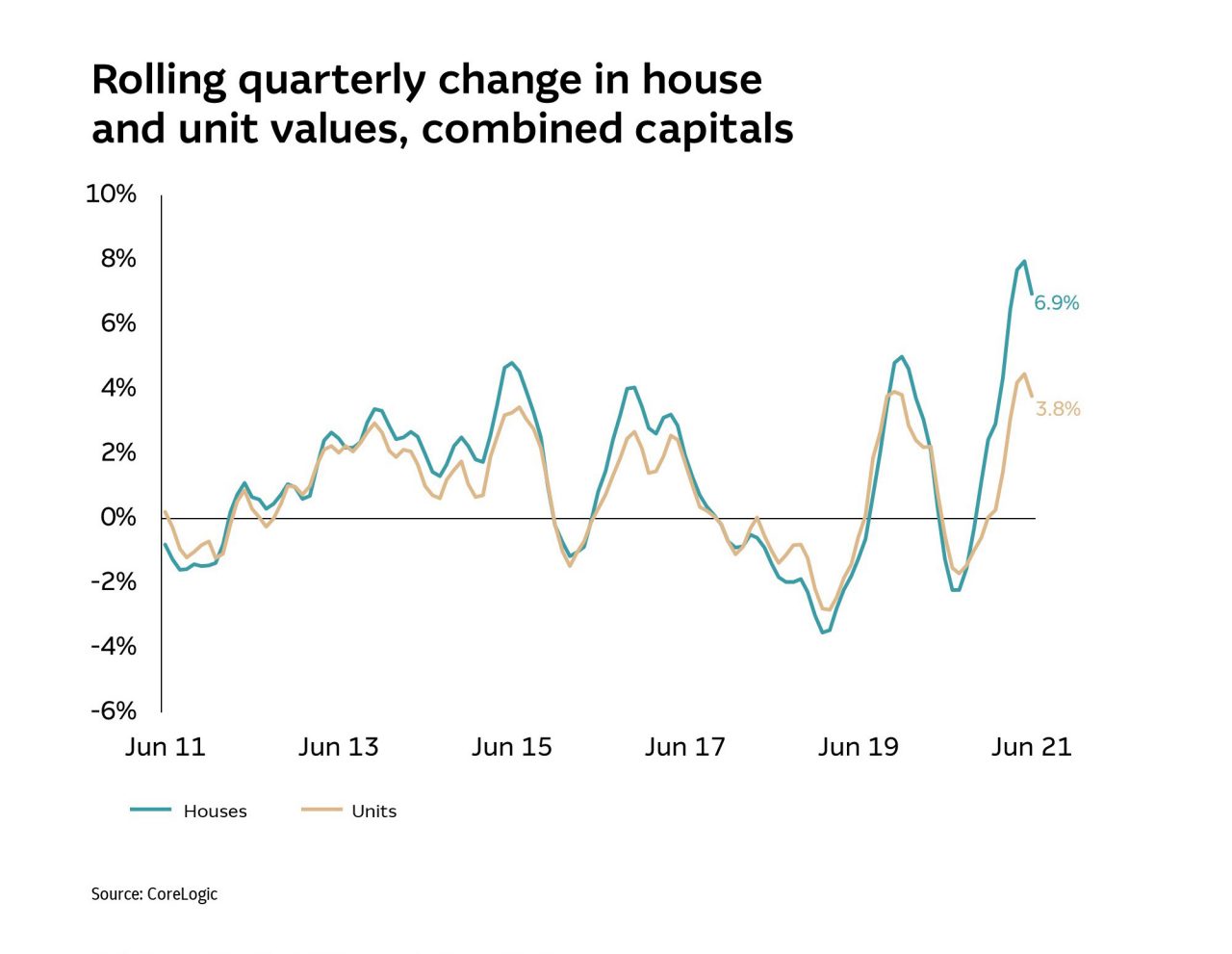

Strong price growth across the capital cities

Strong price growth across the capital cities

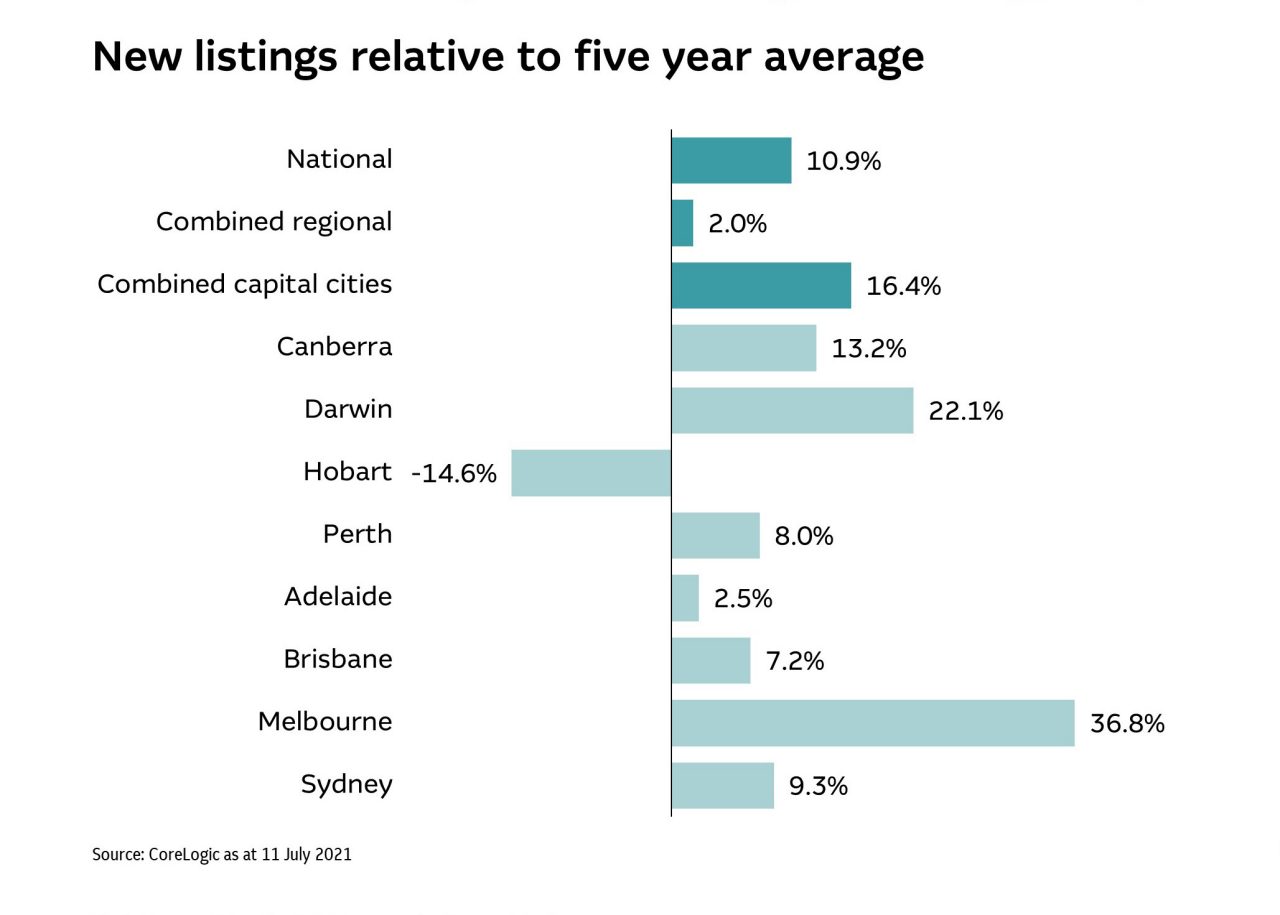

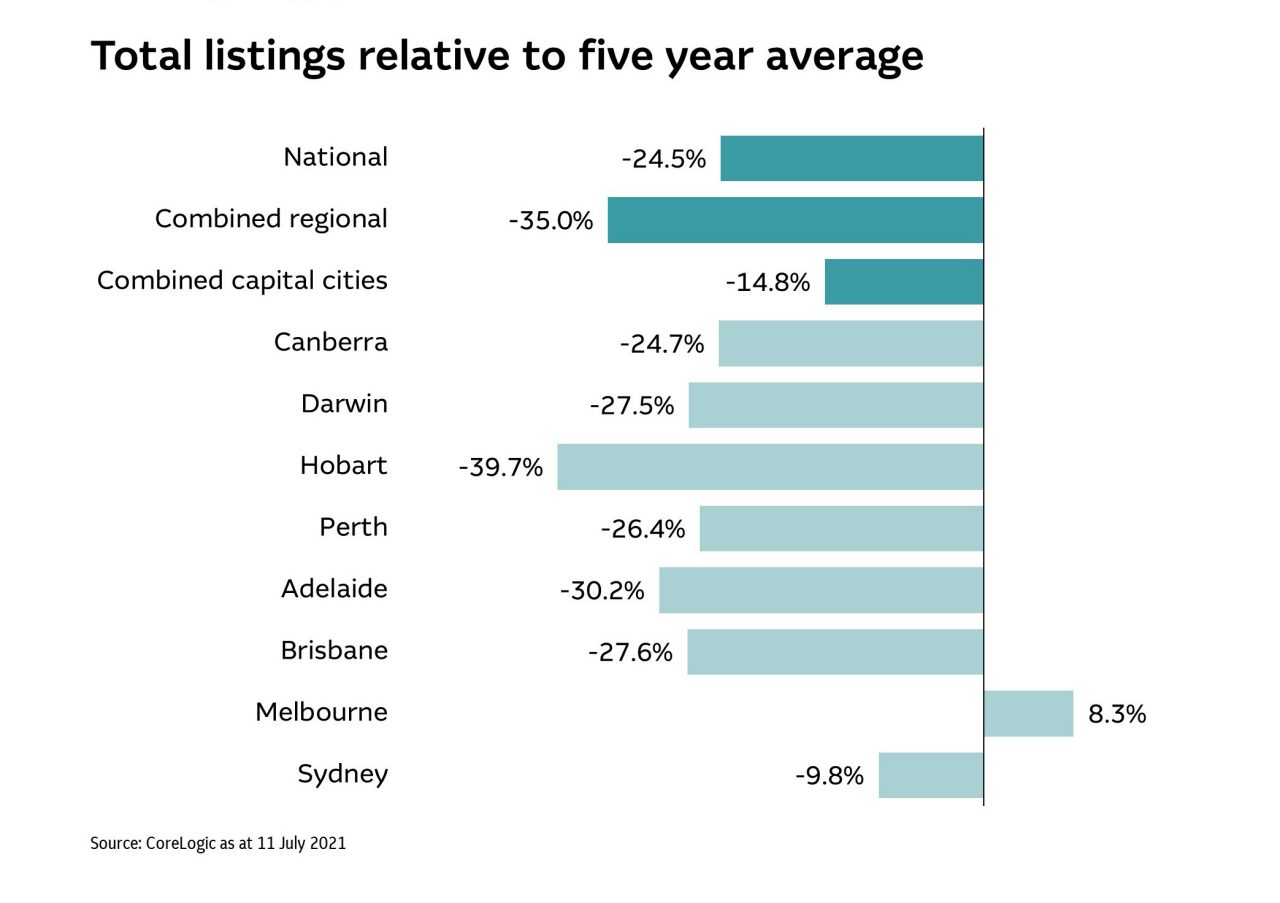

It’s certainly still a ‘seller’s market’, with a continued imbalance between supply and demand. New listings are 10.9% above the five-year average, but the rate of sale is so fast – on average 27 days on market in capital cities – that total listing numbers continue to trend lower, down 24.5% on the five-year average.

A seller’s market: new listings move fast

A seller’s market: new listings move fast

Demand still skewed towards houses

The demand gap continues to widen between houses and units. The six-month house sales trend is tracking 33.7% above the decade average, compared with unit sales rising 19.9%. And this is reflected in value growth. The typical difference between Sydney’s median house value and median unit value is now around 55% – an all-time high. In Canberra, that value gap is as high as 75%.

“With more people able to work remotely, the distance barrier has become less of an issue,” said Stuart. “First-home buyers can see their dollar go a bit further in city fringes, rather than having to compromise on space in a high density option.”

However, over the past six months unit performance has started to improve and affordability constraints may turn buyer attention back to units again.

The house-unit price gap widens

The house-unit price gap widens

Diverging rental returns

The house-unit price gap is also reflected in rental yields. “For example, Sydney house rents are up about 6% over the past year, but down 1.1% for units. In Melbourne this gap is a little more extreme, with house rents up 2.3% and unit rents down 6%,” said Tim.

Rental markets are also diverging geographically with rental conditions stronger outside Melbourne and Sydney – especially inner-city areas. Yields are generally trending lower, with the exception of Perth and Darwin where there was less investment in recent years.

“With mortgage rates so low, there are likely to be some opportunities for positive cash flow investments,” noted Stuart.

Rise of the regions

One of the notable features of this property cycle upswing has been the strength of regional markets. Dwelling values in combined regional areas grew 17.7% over the past 12 months, compared with 12.4% in combined capital cities.

“Values in regional areas rebounded much faster after the lockdowns last year. People moved out of cities into those markets, and regional residents were less likely to move to the capital cities for work or study,” notes Tim.

Lifestyle markets, primarily coastal regions, are still the top performers. Byron Bay is leading the growth surge, with values up nearly 30% year on year. Noosa, Hervey Bay, the Southern Highlands in New South Wales and the Victorian Surf Coast are also proving popular. And with agricultural yields up, markets like Orange, Wagga Wagga and Albury are also making their way into CoreLogic’s Top 30 list.

For business owners re-thinking their CBD commercial footprint, this may also be an opportunity to relocate into those lifestyle areas and tap into new sources of talent.

“This could in turn create more jobs, and even more demand for regional property,” noted Stuart. “Major centres just outside the capital cities, like Newcastle, Wollongong, Geelong, Bendigo, and the Sunshine Coast and Gold Coast, would be well positioned to take advantage of the enduring popularity of flexible working arrangements – especially for knowledge-based sectors.”

Watching out for headwinds

Affordability constraints are likely to be the primary cause of any slowdown in price growth. Credit tightening and interest rate rises could also curb demand, but Stuart and Tim agreed intervention would be unlikely before 2022.

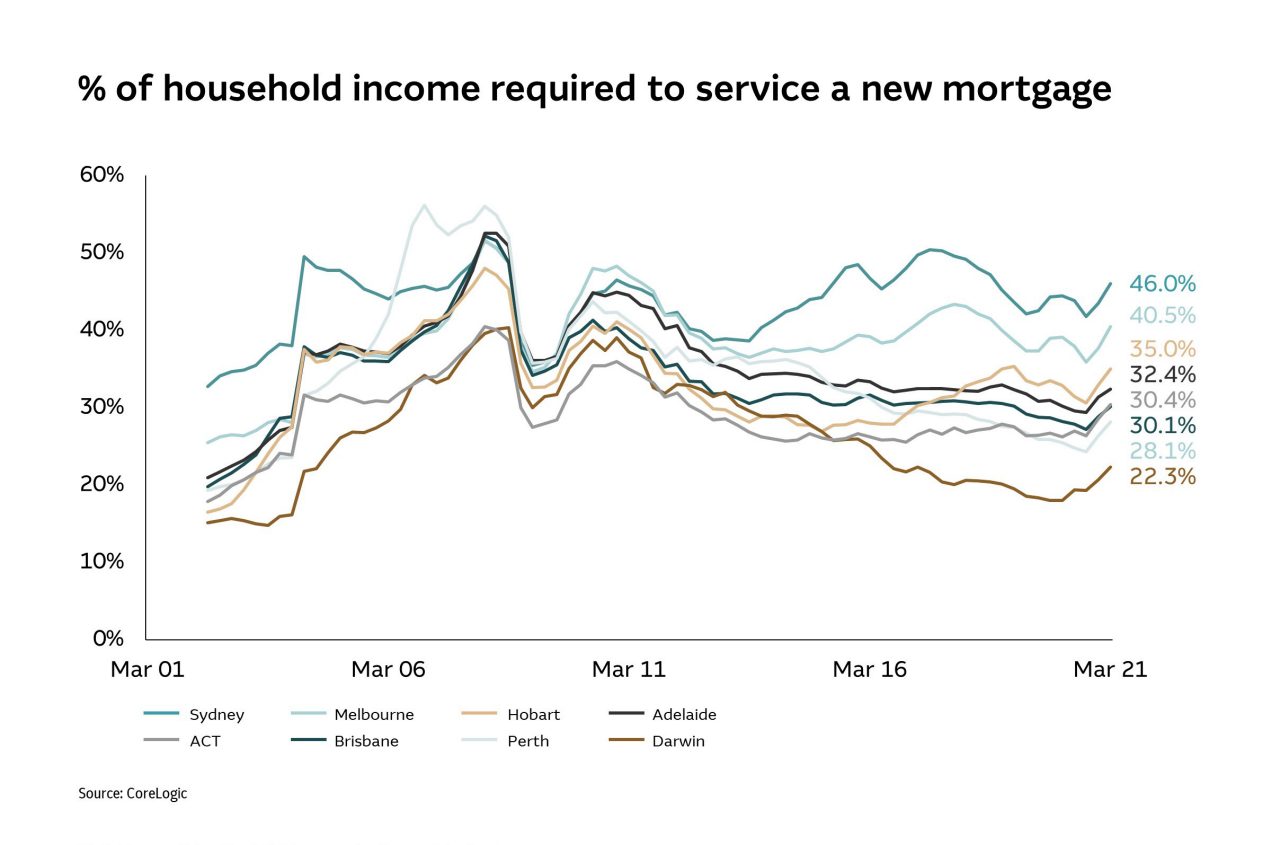

Record highs in housing value to household income ratios

Record highs in housing value to household income ratios

“A lot of clients ask about potential changes to credit policy,” noted Stuart. “The Reserve Bank of Australia and the Australian Prudential Regulation Authority have been clear they won’t shift policy direction simply to tighten the housing market – they will hold until we achieve full employment and inflation is within their target range.”

They may be watching investor lending, which is now outpacing owner-occupier loans as first-home buyers drop back from the market. However, investors are still just 28% of mortgage demand – well below typical levels of around 35%.

“I think we can expect variable interest rates will remain at record low levels,” Stuart added.

Despite the current disruption to transactions due to the recent COVID-19 outbreaks, Tim does not expect it to significantly impact housing growth over the medium-term.

“During the previous ‘circuit-breaker’ lockdowns, we did see new listings fall sharply. It’s harder to inspect properties, and consumer confidence tends to be more volatile. But as restrictions get lifted, things tend to bounce back really quickly,” he said.

Real estate agents will need to be ready to move quickly from ‘pause’ to meeting pent-up demand. And they may need to adapt to more private treaty sales, with CoreLogic data indicating vendors are more likely to accept offers prior to auction in the face of ongoing uncertainty.

“The market still looks strong, so it’s positive news for real estate agents, and it’s still likely to be a seller’s market for some time,” said Stuart.

With foreign buyer purchases almost negligible but likely to bounce back as borders re-open, and the potential for a Brisbane Olympic-fuelled boom, there is still room for optimism in Australia’s residential markets.

To discuss any opportunities for your business, please request a call or speak with your Macquarie Business Banking Relationship Manager.