A budget that reflects the times

- The Albanese Government has delivered a prudent budget, consistent with the need to keep fiscal expenditure expansionary but with the intention of limiting any additional inflationary pressures.

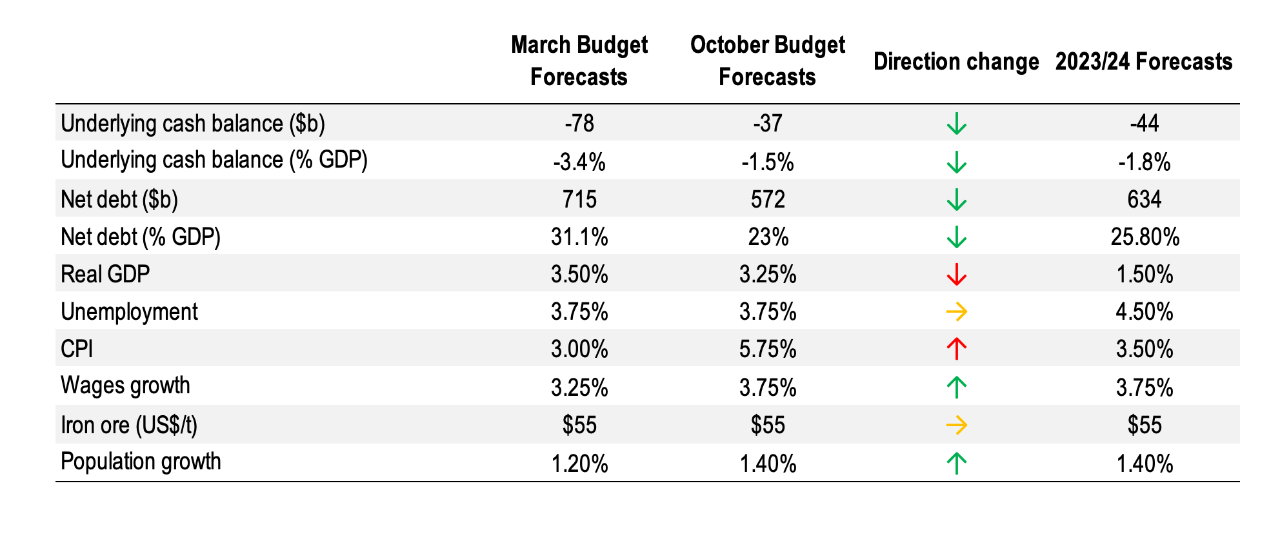

- Treasury is now forecasting a more difficult outlook for the Australian economy. It expects GDP growth to decline to only 1.5% in 2023/24, unemployment to rise by 75bps and for inflation to remain at higher levels out through the next 3 years.

- The primary focus of the budget is to address cost of living pressures. Despite higher tax revenues, the Government has opted to hold on to some of the savings and pursue family-oriented policies that align with the RBA’s goal of bringing inflation back down to its target 2–3% range.

- Who wins? Against a backdrop where economic growth is slowing, but where the fiscal position remains strong, the budget prioritises four key areas with targeted spending addressing: 1) the cost of living; 2) parental and childcare support; 3) infrastructure; and 4) health, education and community services. Companies that are exposed to the housing sector also stand to gain due to the government’s ambitious goal of building around 200,000 affordable homes per year for the next 5 years starting in mid-2024.

- Who loses? This budget did not propose any major long-term reforms that structurally alter the Australian economy. While some modest spending supports environmental restoration and research, a targeted boost to infrastructure and tax breaks for electric vehicles will encourage cleaner transportation, there is little to promote a substantial transition to a more sustainable economy in the near term. In addition, there will be no cash handouts via direct intervention. A cut to the fuel excise will not be reinstated, and cost of living supports will be adjusted via indexation, as opposed to immediate payments.

- This is a very targeted budget. It aims to address the government's long-term debt position, which supports Australia’s AAA credit rating, but does not provide any large-scale fiscal relief. We don’t see it as providing a major boost for the equity market aside from housing and to a lesser extent infrastructure.

- In line with growth downgrades through 2023/24, it removes any upside surprise from government spending. Further, we don’t see the budget providing much additional support for the A$ which is now reliant on interest rate (and to a lesser extent growth) differentials.

Federal Budget 2022/23

This budget primarily focuses on developing a platform for more substantial changes in the economy over the next few years, as opposed to any major reforms in the near term. Given the elevated cost of living, most policies presented in this budget aim to provide relief for households with the intention of limiting any additional momentum to inflationary pressures.

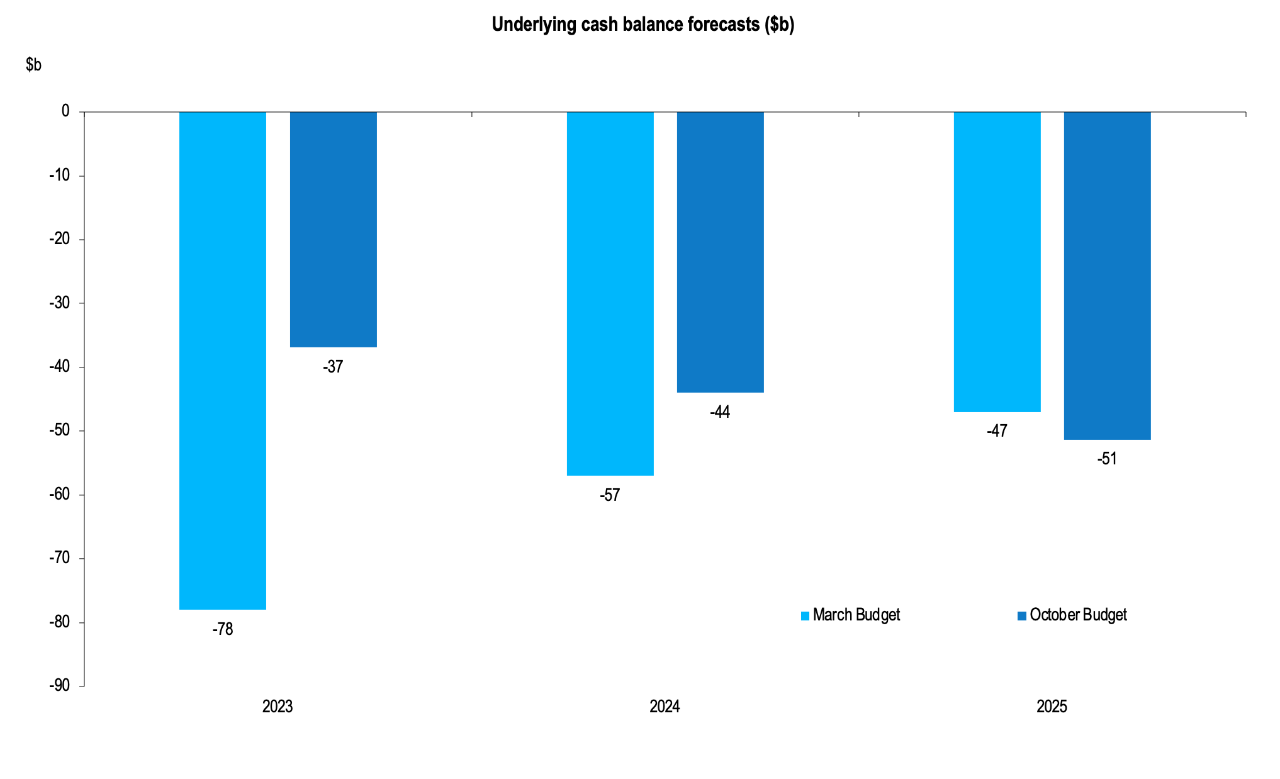

The budget position has improved compared to Treasury’s forecast in March. A combination of a tight labour market, high commodity prices, and a strong rebound in economic activity compared to last year sees the budget deficit declining to $37 billion in 2023 before a modest uptick over the next few years.

An improving budget outcome

Source: Treasury, MWM Research, October 2022

Source: Treasury, MWM Research, October 2022

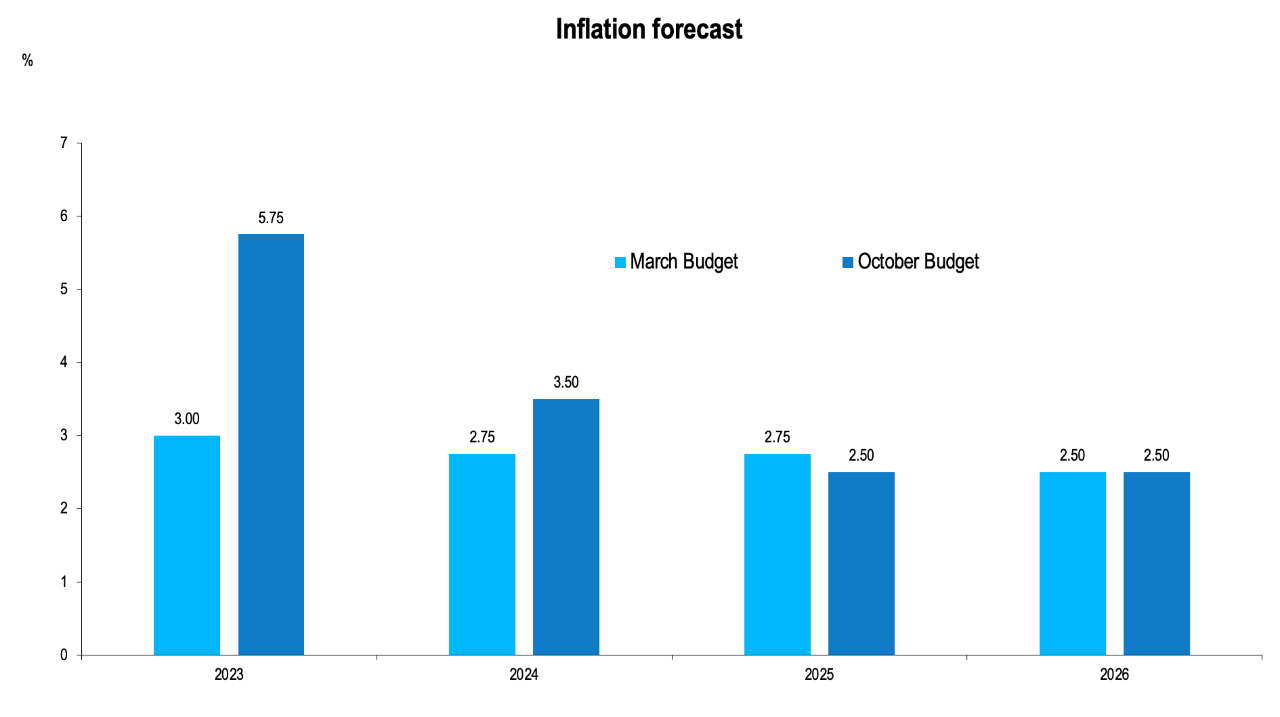

Inflation expectations upgraded: While recent budgets have focused on providing significant stimulus to support households and businesses due to the pandemic, the economic environment now faces the challenge of higher inflation and slowing growth. Treasury forecasts inflation to reach 5.75% by mid-next year, outpacing the March projection of 3.0%. Naturally, if inflation proves to be higher (or stickier) than expected, the budget position may remain in deficit for longer, limiting the flexibility of fiscal spending moving forward.

Inflation is proving to be higher than expected

Source: Treasury, MWM Research, October 2022

Source: Treasury, MWM Research, October 2022

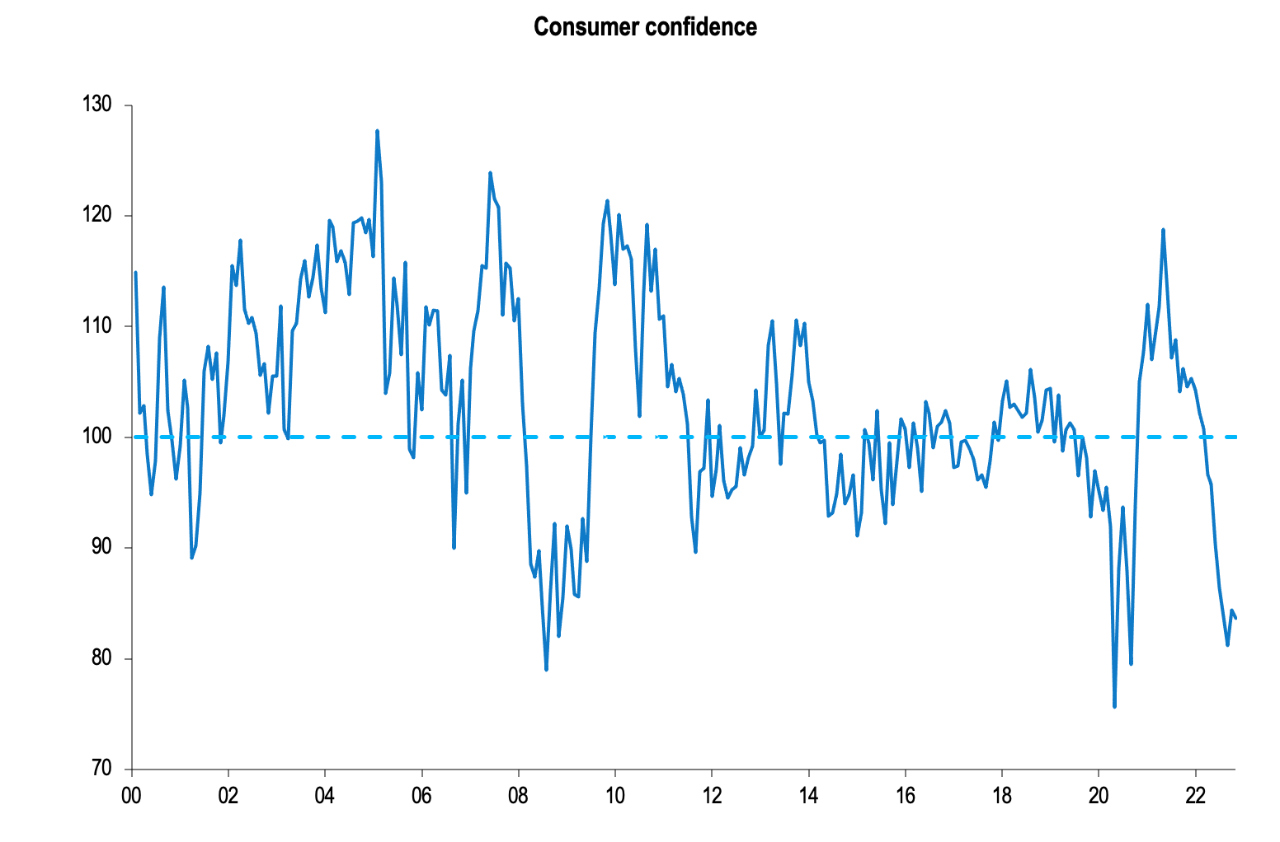

Budget position expected to slightly worsen: The Government has reiterated the need to repair the budget position towards surplus. While 2023 sees a strong improvement compared to the March forecast, the position is expected to slightly deteriorate over the next few years. The focus of this budget has been to cut down on spending and hold on to tax windfalls, instead of raising taxes or halting spending altogether. As such, we do not believe the combination of policies are excessively contractionary (but neither are they excessively expansionary while the RBA is attempting to rein in monetary policy). Nevertheless, there are enough supportive elements that can assist households as economic conditions weaken and confidence declines.

Consumer confidence has continued to decline

Source: Westpac-Melbourne Institute, MWM Research, October 2022

Source: Westpac-Melbourne Institute, MWM Research, October 2022

Growth expectations have been lowered significantly: Treasury is now forecasting a more difficult outlook for the Australian economy. It expects growth will be weaker into 2023/24 with GDP falling to only 1.5% and expect unemployment will be higher by 75bps. However, higher commodity prices are contributing to higher tax revenues which will help ease the deficit, provided they remain strong into a slowing global growth environment.

Treasury forecasts a challenging economic outlook

Source: Treasury, MWM Research, October 2022

Source: Treasury, MWM Research, October 2022

We review the major policy initiatives below.

1. Cost of living pressures

The focus of this budget is to ease the cost of living, albeit, in a manner that does not generate further inflationary pressures. Unlike the previous budget, cost of living supports are largely indexation-based compared to direct cash handouts:

- Social security: Payments to Australians on social security programs will increase by $33 billion over the next four years to mitigate the rising cost of living. This includes higher payments to age pensioners and those receiving JobSeeker payments.

- Stage three tax cuts: The Federal Government has decided to avoid modifying the final stage of proposed tax cuts that will come into effect in 2024. As it stands, the 37% marginal tax rate for those earning over $120,000 will be eliminated. For people earning between $45,000 and $200,000, the 32.5% tax rate will decline to 30%. The top tax bracket (45%) will now apply at $200,000, not $180,000.

2. Parental and childcare support

Addressing the cost of childcare and expanding parental leave are some of the largest commitments in this budget. The Government has also reiterated the importance of increasing female participation in the labour market:

- Paid parental leave: Increasing gradually from 18 to 26 weeks by 2026. The first increase to 20 weeks is marked for 1 July 2023, providing families with more flexibility.

- Parental leave eligibility: Households earning less than a combined $350,000 in income can access paid parental leave, expanding the eligibility criteria that previously depended on an individual income threshold ($150,000). Parents can now also take leave at the same time.

- Cheaper childcare: The maximum subsidy rate will be raised to 90% from 85% for families earning less than $530,000 in household income.

3. Infrastructure

The budget will allocate $9.6 billion towards several nationally significant infrastructure projects including:

- Freight highway upgrades: $1.5 billion allocated for upgrading important highways that facilitate freight including the Tanami, Dukes, and Augusta highways, among others.

- Suburban Rail Link in Victoria: $2.2 billion for the rail system that will connect every major rail line (and the airport) together in Victoria.

- Electrification of public transport in WA: $670 million to manufacture more electric powered buses and battery charging technology in WA.

- Western Sydney roads: $300 million for the development of road linkages in Western Sydney to foster efficient travel of passengers and freight before the new airport opens in 2026.

- NBN: A $2.4 billion investment into the NBN to extend the network to 1.5 million more homes.

4. Health, education and community services

Key initiatives include:

- National Disability Insurance Scheme (NDIS): An increase in funding of $8.8 billion over the next 4 years. An immediate $158.2 million will be made available for hiring 380 permanent staff.

- Aged care reform: $2.5 billion allocated to improve the quality of aged care including an increase in wages for carers and to hire more nurses.

- Cheap medicines: The maximum co-payment on medicines that are included under the Pharmaceutical Benefits Scheme will be reduced by $12.50 to $30.

- TAFE and university: An additional 180,000 fully funded TAFE placements will be made to address skills shortages. For university study, funding will be provided for an additional 20,000 admissions for under-represented students.

- Housing, indigenous and community services: A $560 million pool of funds (reflecting a partial indexation to inflation) will be made available to community organisations that can apply to receive funds over 4 years.

- Housing supply: Under the national Housing Accord, $350 million in funding will be made as a co-investment to kickstart the construction of 10,000 additional affordable homes over the next 5 years, with ongoing payments available over the longer-term as part of the government’s aspiration of building 1 million new homes over the next 5 years. This is in addition to the establishment of the Housing Australian Future Fund, which aims to fund 30,000 new affordable dwellings over 5 years.

Financial market takeaways

This budget reverses the pro-growth agenda that was set out earlier in the year and instead adopts more conservative fiscal policies given the elevated inflationary backdrop and the need to move in the same direction as the RBA.

Traditionally, budgets don’t have a major or prolonged impact on the equity market, and we don’t see the current combination of policies as anything different. Few households or businesses are likely to feel worse off, but, simultaneously, few will feel much better off as any cost-of-living adjustments are quickly absorbed.

We doubt the budget will lift sentiment or confidence in the outlook and in turn it is unlikely to drive households or businesses to raise investment, employment or consumption to any large degree. The intention of the budget is to support areas of weakness – particularly around social security – than to provide a strong lift in aggregate demand. Similarly, we think consumers are more likely to hold on to any gains given ongoing uncertainty around the growth and inflation outlook.

For the bond market, the budget provides some confidence that the Government will not fritter away the gains from high commodity prices even during a time when growth is weak. This reduces inflationary pressures from expansionary fiscal policies, helping keep bond yields relatively supressed and more at the whim of global developments. We think the same can be said for the A$ which is being driven lower by a relatively more muted inflation and interest rate outlook in Australia compared to other advanced economies.

For the equity market, outside of a boost to earnings, we see no reason to think that this budget will have any material impact on the risk premium and/or valuations. This would imply that the forces which have been driving the market throughout the past 6 months (rising bond yields and slowing earnings growth) will remain intact without much of an offset by fiscal policy.

We believe the initiatives aimed at improving access to affordable housing can service as a tailwind for the building and construction linked sector. Potential beneficiaries of this include:

- Developers such as Stockland (SGP) and Mirvac Group (MGR)

- Construction materials suppliers such as ADBRI (ABC), Boral (BLD), Brickworks (BKW), James Hardie Industries (JHX) and Wagners Group (WGN).

- Home fitting suppliers such as GWA Group (GWA) and Reece Ltd (REH).

On a similar note, the consumer spending outlook remains solid heading into the first Christmas period in 3 years where there has been no lockdown restrictions, and this should see a strong spending environment, even if only temporary.

We think the most important drivers of Australia’s financial markets will be the interplay between the following elements:

- Inflation: If prices remain elevated, financial markets will continue to be volatile until there is greater transparency on how services inflation is picking up and when peak rates will be seen.

- Monetary Policy: We believe monetary policy, domestically and abroad, is the most important factor for driving financial market movements. At this stage, and even though the RBA has slowed its pace of rate hikes, further increases are coming with Macquarie expecting the RBA to raise rates by a further 50bps over the next two meetings.

- Global growth momentum: As the outlook for global growth continues to deteriorate, financial markets will continue to be vulnerable to this weakness, particularly as bottom-up earnings expectations remain elevated versus what would be expected during a period of slowing economic growth.

We remain cautious on the Australian equity market and see little chance that it will break with the direction of global markets. This budget is neither positive nor negative for the market, barring housing-linked stocks, and we think its impact will not be long-lasting as investors settle back and refocus on the same drivers that have been impacting markets since the start of the year.

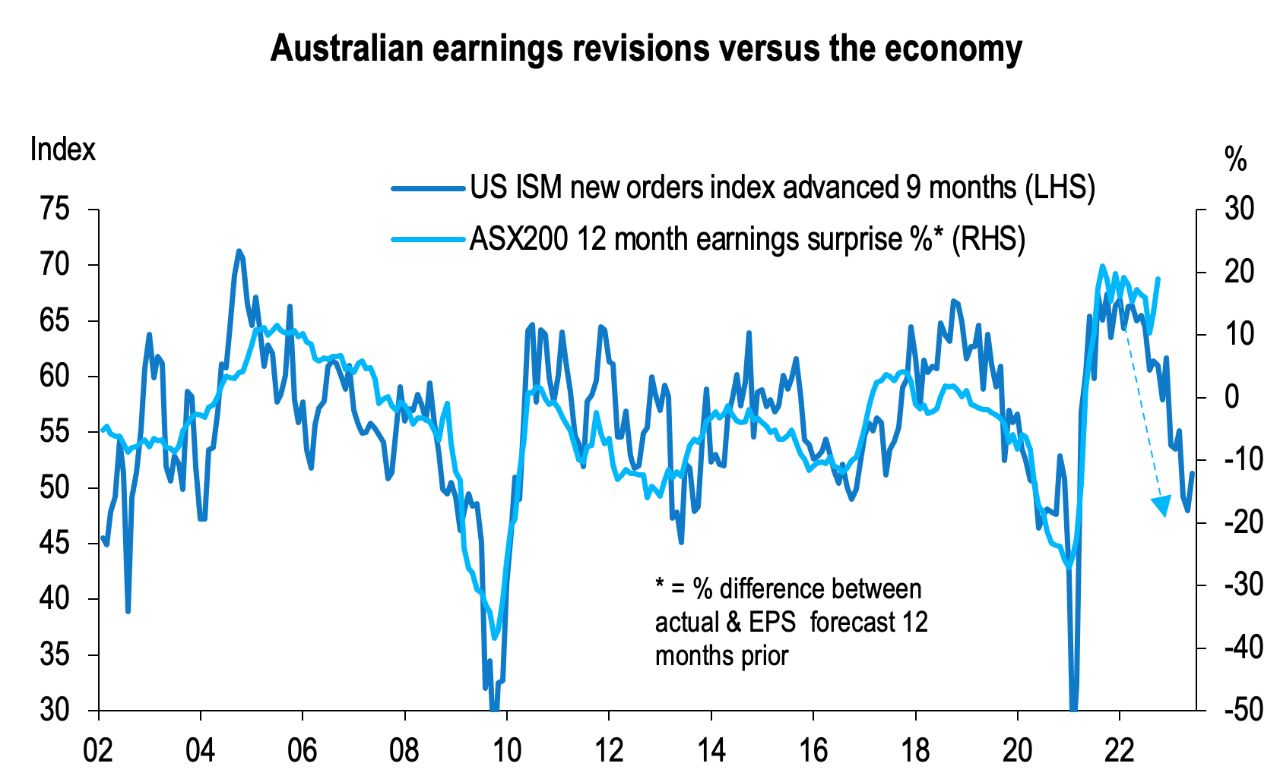

Australian equity earnings depend on the global economy

Source: FactSet, MWM Research, October 2022

Source: FactSet, MWM Research, October 2022

Macquarie WM Investment Strategy Team